Based in: Urb. Belisa, #1532A Calle Bori, San Juan, PR, 00927

Warning: Undefined variable $height in /customers/4/2/e/mybusinessbid.com/httpd.www/wp-content/plugins/pt-unta-addons/shortcodes/banner-slider.php on line 490

News Business & Owners Strategies CPA’s LLC – News November 20, 2020

IRS issued final guidance on PPP:

Rev. Rul. 2020-27 / May a taxpayer that received a loan guaranteed under the Paycheck Protection Program (PPP) authorized under section 7(a)(36) of the Small Business Act (15 U.S.C. 636(a)(36)) (covered loan), and paid or incurred certain otherwise deductible expenses listed in section 1106(b) of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act)…

Rev. Proc 2020-51 / This revenue procedure provides a safe harbor allowing a taxpayer to claim a deduction in the taxpayer’s taxable year beginning or ending in 2020 (2020 taxable year) for certain otherwise deductible eligible expenses, as defined in section 2.03 of this revenue procedure…

En un foro convocado por el Fideicomiso de Ciencia trascendió que, gracias a tecnología israelí, el laboratorio CorePlus en Carolina usa inteligencia artificial para diagnosticar cáncer de próstata con mayor precisión

Una relación comercial de “mofongo con humus” ha permitido que el laboratorio de servicios clínicos y patológicos CorePlus en Carolina esté usando inteligencia artificial (IA), desarrollada por la startup israelí IBEX Technologies, para ofrecer 99.6% de precisión en el diagnóstico del cáncer de próstata.

Así bautizó el principal ejecutivo de CorePlus, Mariano De Socarraz, la alianza que concretó el año pasado con su homólogo de IBEX, Joseph Mossel, luego de enterarse en una publicación académica del desarrollo de una tecnología que, a su juicio, “transforma la patología” por incorporar IA a un campo que por unos 100 años ha dependido de observaciones hechas por humanos.

“Vimos una misión mucho más grande, no solo una oportunidad de negocio, en una industria que no cambia con tanta rapidez”, comentó De Socorraz. “Creo que somos los únicos en las Américas que usamos esta tecnología siempre en nuestras pruebas diagnósticas de próstata”.

El acuerdo entre CorePlus e IBEX Technologies se presentó ayer como un caso de éxito sobre las posibilidades de fraguar relaciones comerciales entre empresas establecidas o emergentes de Israel y Puerto Rico, en un evento convocado por el Fideicomiso de Ciencia, Tecnología e Investigación.

Durante el foro participó también el puertorriqueño Javier Soltero, vicepresidente de Google Workspace, quien profundizó en cómo la pandemia ha escalado la adopción de herramientas digitales pues, antes de esta crisis sanitaria, “la transformación digital era algo que se podía contemplar y planear y traer paso a paso. Entre febrero y marzo, básicamente se convirtió en necesidad y urgencia”.

Ahora, tras meses de estabilizarse la transición a una vida de trabajo, educación y recreo remotos, Soltero opinó que uno de los retos que persisten es crear soluciones que incorporen un poco del calor humano que falta en las interacciones.

“Lo más importante después de la pandemia es la evidencia de que pudimos hacerlo, pudimos operar negocios y sistemas educativos. Retos los hubo y los habrá. Pero hay evidencia ahora de que es posible operar un banco todo el mundo desde sus casas. El mundo no paró”, reflexionó Soltero.

De cara a un futuro híbrido, expresó la aspiración de que algunas cosas no vuelvan a lo que se veía normal, sino que persista “un sentido de corrección en casi todos los sectores de la economía”, que va a ser potenciado por las conductas y formas de hacer las cosas que ya han cambiado. Como ejemplo, propuso algo tan sencillo como el uso de QR Codes para ver menús, que reduce la necesidad de usar materiales que luego se desechan. “Ese tipo de digitalización de las experiencias, que se dan también en manufactura, logística, se va a mantener con nosotros”.

¿Cómo luce el ecosistema de innovación en Israel?

Por su parte,Ben Yaron, gerente de desarrollo de negocio de Start-up Nation Central de Israel, detalló que en ese país se ve la mayor densidad de emprendimientos tecnológicos, ya que hay “1 startup por cada 1,400 personas”.

Pero, como se trata de un país diminuto, con menos de 9 millones de habitantes, “no hay mercado” y los emprendedores se dedican a desarrollar soluciones para los grandes retos globales en empresas y poblaciones fuera de sus fronteras. Los campos de mayor desarrollo, según indicó, son agricultura, agua, energía, software, ciencias vivas, telecomunicaciones, ciencias de datos, ciberseguridad e internet de las cosas (iOT).

Por ello, el ecosistema de innovación de Israel es esencialmente B2B (de empresas que desarrollan soluciones y productos para otras empresas).

“En Israel no tiene sentido crear mucho B2C (productos y servicios para consumidores) porque estamos lejos de poblaciones amplias y rodeados de países que no son amigos”, recalcó.

Las grandes empresas foráneas no han pasado por alto estas realidades, aseguró Yaron, porque ya el ecosistema israelí cuenta con cerca de 350 centros internacionales de investigación y desarrollo y la presencia de 220 fondos de capital privado. También se nutre con 22 incubadoras y más de 100 aceleradoras.

Las empresas prevén otorgar un incremento salarial del 39% en 2020 para el personal fuera de convenio, con una inflación anual estimada del 41,3%, según el relevamiento realizado por la consultora Mercer, especializada en Recursos Humanos, entre 342 empresas. Este porcentaje muestra una baja de 1,7 puntos porcentuales desde la medición de marzo, previa a la pandemia.

Un trabajo de la consultora Willis Towers Watson sobre 389 empresas arrojó que el incremento promedio previsto para los empleados fuera de convenio era de 36,3%.

Según Mercer, el aumento efectivamente otorgado hasta julio equivale a un 20% mientras que la inflación acumulada hasta este mes es del 16%. “Esta situación responde al efecto de la retracción de la inflación: las empresas y los economistas privados creen que la inflación está contenida por la situación de cuarentena todavía vigente. La inflación según fuentes oficiales y privadas estaría en el orden del 41,3% anual”, explicó Ivana Thornton, Directora de Career de Mercer.

Los aumentos salariales previstos por las empresas para el 2020 difieren en función de la industria. Las compañías del sector de Fintech darán 42,7%; mientras que en High Tech se otorgará 41,8%; en Retail o comercio minorista darán 40,4%; en Consumo Masivo, 40,2% y en Agro, 40,1%. Ciencias de la Vida (40%) y Automotriz (40%) completan el cuadro de industrias que superan la mediana de mercado (39%).

Por otro lado, las industrias de Energía (23,3%), Ingeniería y Construcción (28,8%), Servicios (34,1%) y Bancos (26%) se ubican por debajo en el ranking de aumentos anuales previstos.

Por otra parte, las empresas están cambiando su cronograma de aumentos, estirándolo hacia los últimos meses del año.

El 41% de las empresas encuestadas señaló que dará dos incrementos; el 29% otorgará tres; el 18% otorgará cuatro; el 10,5% dará uno solo y el 1,5%, ninguno.

El 8% de las empresas no otorgaron ningún incremento entre enero y agosto de este año. De este 8%, el 82% estima otorgar un incremento del 25% entre septiembre y diciembre y el 18% restante no otorgará incrementos.

“Dado el contexto, no se puede afirmar con exactitud que los incrementos proyectados para lo que queda del año realmente sucedan. Las empresas esperan otorgarlos pero la evolución de los negocios será la variable determinante”, detalló la experta.

Con respecto a la proyección para 2021, sólo un 29% de las organizaciones respondieron tener un estimado de incrementos salariales siendo este del 40% anual, con una inflación estimada del 40,6 para el próximo año.

Lo mismo sucede con el sondeo de Willis Towers Watson: solo 33% hizo el presupuesto para el año que viene. Y la estimación del aumento es de 39,3%.

Si tienes un negocio, qué debes saber para “salvarlo” y que funcione post-pandemia

Fuente: MSN

La pandemia de coronavirus está reinventando a todas las empresas para buscar nuevas y rápidas fuentes de ingresos para mantener los negocios a flote.

Es el momento adecuado para pensar cómo será el mundo después de la pandemia. Si tienes un negocio estas preguntas serán necesarias para diseñar una estrategia de recuperación rápida según el sitio Inc.:

¿Cómo cambiará la vida de tus clientes?

Los cambios de la pandemia están creando nuevas necesidades por lo que será entregar valor a tus clientes será la clave.

Anticipate cómo necesitarás cambiar tus productos y servicios o crear nuevos para ofrecer un valor agregado a tus productos.

¿Qué pasará con tu competencia actual?

Recuerda que tu competencia también hará cambios para poder sobrevivir a la pandemia. Deberás hacer suposiciones financieras de tu competencia y los movimientos estratégicos que realizará.

¿Quién será tu nueva competencia?

También tendrás que considerar quién podría unirse al mismo rubro de negocio en el que te desempeñas.

Deberás evaluar quién ya está en el mercado y revisar las estrategias que los demás estén haciendo para conocer todos los movimientos.

¿Dónde contratarás nuevos trabajadores?

Con el despido de más de 26 millones de personas en el país, al perder una gran cantidad de fuerza de trabajo necesitarás reconstruir un plan para conseguir de manera rápida a los mejores talentos antes de que las demás empresas apuesten por ellos.

¿Cómo será la cadena de suministro?

Cuando tu negocio depende de proveedores, será necesario revisar de manera cuidadosa la cadena de suministro y revisar qué es lo que funciona y que no.

Realiza un plan de apoyo para tu recuperación y crecimiento de tu negocio.

¿Qué diferenciará a tu negocio en el nuevo mercado?

Una vez que cuentes con un plan enfocado a tu cliente principal, tu producto o servicio, tendrás que evaluar cómo conseguirás el mercado.

Las mejores empresas cuentan con una estrategia de diferenciación que las hace únicas frente a su competencia.

De lo contrario, estarás compitiendo por el precio y este no es un buen momento. Deberás identificar dos o tres factores que te hacen destacar entre tus clientes.

¿Qué necesitarás implementar o dejar de hacer?

Durante tu revisión deberás averiguar qué capacidades necesitarás dejar de hacer. Cuando las identifiques deberás asignar tus recursos a nuevas estrategias.

¿Cuáles son los pronósticos mensuales?

Ya que tengas un posicionamiento deberás hacer un pronóstico para los próximos 12 y 24 meses con los objetivos operativos.

También necesitarás una clave para implementar cualquier cambio en los negocios y construcción de nuevas capacidades que serán clave para establecer prioridades.

Trabajar en medio de una crisis no es fácil y puede ser angustioso para muchas personas.

Entre más rápido estabilices tu situación actual y observes cómo será el nuevo comportamiento del mercado, no solo tendrás mayores posibilidad de éxito en el futuro, sino que también tendrás la confianza y motivación para seguir adelante ante cualquier eventualidad.

Farmers and Fishermen – File your 2019 income tax return (Form 1040) and pay any tax due. However, you have until April 15 to file if you paid your 2019 estimated tax by January 15, 2020.

Health Coverage Reporting – If you are an Applicable Large Employer, provide Form 1095-C, Employer-Provided Health Insurance Offer and Coverage, to full-time employees. For all other providers of minimum essential coverage, provide Form 1095-B, Health Coverage, to responsible individuals.

Large Food and Beverage Establishment Employers – with employees who work for tips. File Form 8027, Employer’s Annual Information Return of Tip Income and Allocated Tips. Use Form 8027-T, Transmittal of Employer’s Annual Information Return of Tip Income and Allocated Tips, to summarize and transmit Forms 8027 if you have more than one establishment. If you file Forms 8027 electronically your due date for filing them with the IRS will be extended to March 31.

March 10

Employees who work for tips – If you received $20 or more in tips during February, report them to your employer. You can use Form 4070.

March 16

Employers – Nonpayroll withholding. If the monthly deposit rule applies, deposit the tax for payments in February.

Employers – Social Security, Medicare, and withheld income tax. If the monthly deposit rule applies, deposit the tax for payments in February.

Partnerships – File a 2019 calendar year income tax return (Form 1065). Provide each partner with a copy of their Schedule K-1 (Form 1065-B) or substitute Schedule K-1. To request an automatic 6-month extension of time to file the return, file Form 7004. Then file the return and provide each partner with a copy of their final or amended (if required) Schedule K1 (Form 1065) by September 15.

S Corporations – File a 2019 calendar year income tax return (Form 1120S) and pay any tax due. Provide each shareholder with a copy of Schedule K-1 (Form 1120S), Shareholder’s Share of Income, Credits, Deductions, etc., or a substitute Schedule K-1. If you want an automatic 6-month extension of time to file the return, file Form 7004 and deposit what you estimate you owe in tax.

S Corporation Election – File Form 2553, Election by a Small Business Corporation, to choose to be treated as an S corporation beginning with calendar year 2020. If Form 2553 is filed late, S corporation treatment will begin with calendar year 2021.

March 31

Electronic Filing of Forms – File Forms 1097, 1098, 1099 (except Form 1099-MISC), 3921, 3922, and W-2G with the IRS. This due date applies only if you file electronically. The due date for giving the recipient these forms generally remains January 31.

Electronic Filing of Form W-2G – File copies of all the Form W-2G (Certain Gambling Winnings) you issued for 2019. This due date applies only if you electronically file. The due date for giving the recipient these forms remains January 31.

Electronic Filing of Forms 8027 – File copies of all the Forms 8027 you issued for 2019. This due date applies only if you electronically file.

Electronic Filing of Forms 1094-C and 1095-C and Forms 1094-B and 1095-B – If you’re an Applicable Large Employer, file electronic forms 1094-C and 1095-C with the IRS. For all other providers of minimum essential coverage, file electronic Forms 1094-B and 1095-B with the IRS.

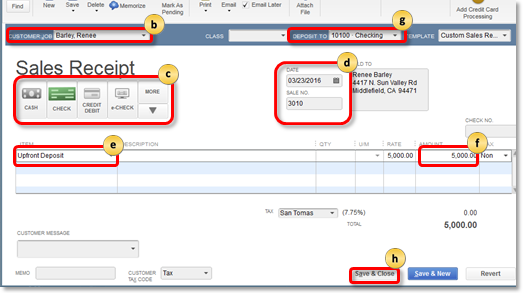

Recording payments, whether they come in to comply with an invoice you sent or are issued as sales receipts, is one of the more satisfying tasks you do in QuickBooks. The sales cycle is almost complete, and you’re about to have more money in the bank – once you document the payments as bank deposits.

Unless you use QuickBooks Payments, which moves your company’s remittances into an account automatically, you’ll have to deal with your deposits twice. First, you’ll have to make out a deposit slip for the bank. You’ll also need to record the deposit in QuickBooks itself.

Fortunately, the software makes this easy for you. Here’s how it works.

A Special Account

By default, QuickBooks transfers payments received into an account called Undeposited Funds. You can see it in your Chart of Accounts by clicking the Chart of Accounts icon on QuickBooks’ home page and scrolling down a bit. Look over to the end of the line and you’ll see its current balance. This account is an Other current asset. It holds your payments until you record them as deposits and take your money to the bank.

When you’re getting ready to take cash and checks to the bank, click the Record Deposits icon on the home page. The Payments to Deposit window will open.

Figure 1: When money moves into Undeposited Funds from invoice payments or sales receipts, it’s displayed in the Payments to Deposit window.

We recommend completing your physical deposit slip first, based on the checks and cash you have in hand. Then, match them to payments in the window pictured above. You can click in front of each one you’ve matched to create a checkmark. When you’ve finished, click OK. The Make Deposits window will open. Make sure that the account you want to Deposit to is showing in the upper left corner. You can add a Memo and change the Date if needed.

Do you want cash back from your deposit? You may want to move this to Petty Cash, for example. Click the down arrow in the Cash goes back to field and select the correct account. Add a memo if necessary and enter the Cash back amount. When you’re done, save the transaction. QuickBooks now knows that you’re taking a deposit slip to the bank.

The total for your handwritten deposit slip and the final tally in the Make Deposits window should be the same. This will ensure that the amount deposited in your bank account will match the bank deposit amount in QuickBooks when reconciling. If you have leftover cash or checks, you’ll need to track down their origins and create new transactions.

Checking Your Work

It’s a good idea to check your Undeposited Funds account occasionally to make sure that you haven’t left money undeposited. To do this, open your Chart of Accounts again. Right-click Undeposited Funds and click on QuickReport: [number] Undeposited Funds. All should be selected in the Date field in the upper left. Click on Customize Report and select the Filters tab. Scroll down in the Filters list and click on Cleared. Select No and click OK to display your report.

Figure 2: You can customize your QuickReport to see if you’ve neglected to deposit any payments. If this list contains any, open the Banking menu and select Make Deposits to follow the steps above again.

Changing Your Destination Account

As we’ve already mentioned, QuickBooks is set up to automatically move payments into Undeposited Funds. We recommend leaving it this way so you can easily check for money that hasn’t been deposited. You can change this, though. If you feel it’s necessary, please call the office and speak to a QuickBooks professional who will help you modify your destination account.

Working with Payment Methods

QuickBooks comes with a default set of payment methods. You can add to these and/or make existing ones inactive, so they don’t clutter up the drop-down list. Open the Lists menu and select Customer & Vendor Profile Lists | Payment Method List. If you don’t accept Discover cards, for example, right-click on that entry and select Make Payment Method Inactive. To add one, click the down arrow next to Payment Method and then New. The Payment Method should always match the Payment Type.

Precision Critical

Account reconciliation is difficult enough without having to deal with deposit discrepancies. Treat this element of your accounting with great care. If you need help with account management, financial reporting or any other QuickBooks-related issues don’t hesitate to call.

The short answer is yes, tips are taxable. If you work at a hair salon, barbershop, casino, golf course, hotel, or restaurant, or drive a taxicab, then the tip income you receive as an employee from those services is taxable income. Here are a few other tips about tips:

Taxable income. Tips are subject to federal income and Social Security and Medicare taxes, and they may be subject to state income tax as well. The value of noncash tips, such as tickets, passes, or other items of value, is also income and subject to federal income tax.

Include tips on your tax return. In your gross income, you must include all cash tips you receive directly from customers, tips added to credit cards, and your share of any tips you receive under a tip-splitting arrangement with fellow employees.

Report tips to your employer. If you receive $20 or more in tips in any one month, you should report all your tips to your employer. Your employer is required to withhold federal income, Social Security, and Medicare taxes.

Keep a daily log of your tip income. Be sure to keep track of your tip income throughout the year. If you’d like a copy of the IRS form that helps you record it, please call.

Tips can be tricky. Don’t hesitate to contact the office if you have questions.

The Taxpayer Certainty and Disaster Tax Relief Act, passed on December 20, 2019, includes several provisions that may apply to tax-exempt organizations’ current and previous tax years. As such, tax-exempt organizations should understand how these recent tax law changes might affect them. With this in mind, let’s take a look at three key pieces of legislation that affect nonprofit organizations:

1. Repeal of “parking lot tax” on exempt employers

This legislation retroactively repealed the increase in unrelated business taxable income by amounts paid or incurred for certain fringe benefits for which a deduction is not allowed, most notably qualified transportation fringes such as employer-provided parking. Previously, Congress had enacted this provision as part of the Tax Cuts and Jobs Act, effective for amounts paid or incurred after December 31, 2017.

Tax-exempt organizations that paid unrelated business income tax on expenses for qualified transportation fringe benefits, including employee parking, may claim a refund. To do so, they should file an amended Form 990-T within the time allowed for refunds.

2. Tax simplification for private foundations

The legislation reduced the 2% excise tax on net investment income of private foundations to 1.39%. At the same time, the legislation repealed the 1% special rate that applied if the private foundation met certain distribution requirements. The changes are effective for taxable years beginning after December 20, 2019.

3. Exclusion of certain government grants by exempt utility co-ops

Generally, a section 501(c)(12) organization must receive 85% or more of its income from members to maintain exemption.

Under changes enacted as part of the Tax Cuts and Jobs Act, government grants are usually considered income and would otherwise be treated as non-member income for telephone and electric cooperatives. Under prior law, government grants were generally not treated as income, but as contributions to capital.

Certain government grants made to tax-exempt 501(c)(12) telephone or electric cooperatives for purposes of disaster relief, or for utility facilities or services, are not considered when applying the 85%-member income test. Since these government grants are excluded from the income test, exempt telephone or electric co-ops may accept these grants without the grant impacting their tax-exemption. The 2019 legislation is retroactive to taxable years beginning after 2017.

Form 8962, Premium Tax Credit, reconciles 2019 advance payments of the premium tax credit and may also affect a taxpayer’s ability to get advance payments of the premium tax credit or cost-sharing reductions. Taxpayers who don’t file and reconcile their 2019 advance credit payments may not be eligible for advance payments of the premium tax credit in the future. Furthermore, filing Form 8962, with a return avoids possible delays in processing tax returns and subsequent delays in receiving tax refunds.

Background

The premium tax credit helps pay for health insurance coverage bought from the Health Insurance Marketplace. When the taxpayer or their family member applies for coverage, the marketplace estimates the amount of the premium tax credit they may be able to claim. This estimate is based on information the taxpayer provides about family size and projected household income. The taxpayer can then decide if they want to have all, some, or none of the credit paid directly to their insurance company. This option will lower their monthly payments.

Who needs to file Form 8962?

Taxpayers who have advance credit payments made on their behalf are required to file Form 8962 with their income tax return. This will reconcile the amount of advance payments with the premium tax credit they may claim based on their actual household income and family size.

Reconciling advance credit payments

Taxpayers or members of their family who enrolled in health insurance coverage for 2019 through the marketplace should receive Form 1095-A, Health Insurance Marketplace Statement. This form shows the months of coverage and amount of any Advanced Premium Tax Credit (APTC) paid to the taxpayer’s insurance company. This form also provides information needed to complete Form 8962.

Taxpayers should figure their premium tax credit and compare it to the amount of APTC on Form 8962, then file Form 8962 with their tax return.

Taxpayers who received advance credit payments must file a tax return to reconcile even if they otherwise don’t have to file.

Please call the office if you have any questions about this or any other topic affecting your tax return.